APRIL 2026 MARKET REVIEW

Markets, it turns out, are not good readers of headlines. Following a volatile March, April gave investors every reason to stay concerned: the Strait of Hormuz remained disrupted, oil prices hit crisis levels, and diplomatic efforts to de-escalate the U.S.-Iran conflict repeatedly stalled. Yet global equities staged one of the strongest monthly rallies in memory, reversing March’s weakness to close at all-time highs, as the asset class table highlights. Markets looked through the noise, anchoring on what matters most: corporate earnings trajectory and the durability of the AI theme.

Emerging markets were especially notable, helped by strength in key economies tied to the global AI supply chain. The region has continued to show characteristics consistent with a long-term inflection point, and the weakness in March provided an opportunity to further align our positioning with a more constructive outlook.

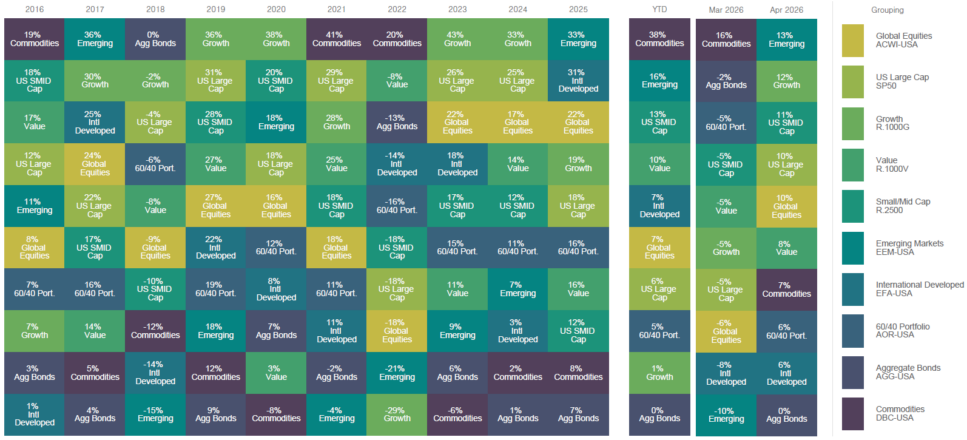

The asset class performance “quilt” included below highlights returns across a range of asset classes over the past 10 years. While leadership shifts meaningfully from year to year, the quilt illustrates how diversified portfolios have historically helped smooth returns over full market cycles.

Source: FactSet, as of April 30, 2026

April Market Highlights

- Emerging markets led all major asset classes with a 13% return in April, marking a sharp reversal from March when the region was the weakest laggard at approximately -10%.

- Semiconductors drove the tech-heavy Nasdaq-100 to register its best monthly performance in more than 23 years (October 2002).

- US Small and Mid-Cap (SMID) equities returned 11%, outperforming large-cap stocks as market breadth continued to expand.

- Commodities gained 7% in April and remain the clear year-to-date leader with a 38% total return.

- Following a difficult March, aggregate bonds stabilized at 0% for the month.

The Power of Corporate Profits

The primary driver of this resilience is corporate results, specifically the massive tailwind from the global AI investment cycle. 1For the first quarter of 2026, the blended earnings growth rate for the S&P 500 is currently tracking at 27.1% (Source: FactSet Earnings Insight, May 1, 2026). If this holds, it will mark the highest earnings growth rate reported by the index since 2021. This momentum is being led by technology and semiconductors, which have reasserted themselves as the market’s primary engines.

AI has become the dominant theme of this bull market, acting as a powerful engine for profitability and margin resilience. Since the beginning of the year, forward earnings estimates have been revised higher (meaning analysts have increased their forecasts for future profitability) by 11%, representing one of the strongest upward revisions witnessed in recent decades (Source: FactSet Earnings Insight, May 1, 2026). Despite geopolitical and inflationary shocks, corporate profits remain the north star of this cycle, providing a fundamental anchor even as the journey forward remains anything but a straight line.

The Emerging Markets Inflection Point

Several structural pillars have shifted positively for emerging markets, prompting our more constructive outlook. The global AI buildout has shifted the center of gravity for technology hardware toward Asia, with markets like Taiwan and South Korea acting as essential manufacturers. Additionally, emerging market valuations remain attractive relative to their 20-year averages, even as regional earnings revisions reach their strongest levels in years.

We are also encouraged by a growing focus on corporate governance across key EM economies. Several countries are implementing significant reforms to improve capital efficiency and become more shareholder-friendly. Programs aimed at incentivizing higher dividends and stock buybacks are helping to narrow the valuation discount that has historically weighed on these markets.

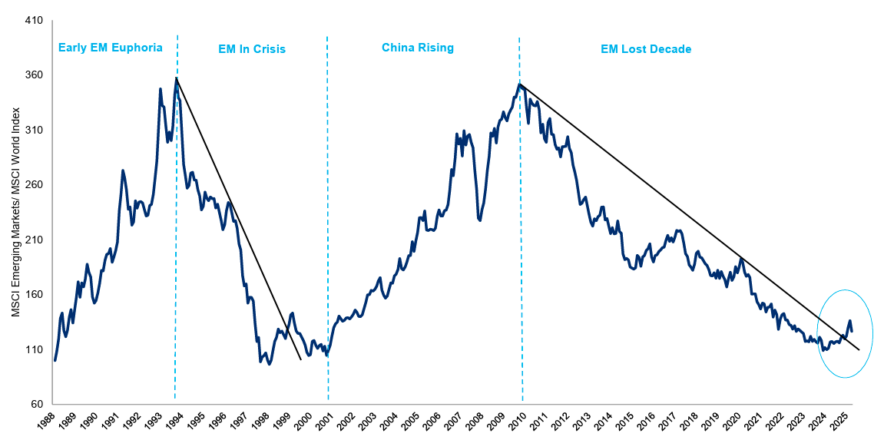

This shift is now visible in the price action. As shown in the chart below, it’s our opinion that emerging markets are attempting to break out from a “Lost Decade” of underperformance relative to developed markets. From a “wisdom of the crowds” perspective, this breakout suggests the market is finally aggregating these fundamental strengths into what may be the very early phase of a regime shift.

Emerging Markets vs Developed Markets Relative Performance Since 1989

Source: RBC Global Asset Management, MSCI, Bloomberg, March 2026, black trendlines drawn by Les Vasvari, CFA, CMT

Closing Thoughts

April’s performance serves as a reminder that while headlines capture our attention, we serve ourselves better by focusing on them less and on the underlying fundamentals more. Success in this environment requires the discipline to look past the immediate noise and recognize the structural trends currently at play. While volatility is the unavoidable cost of entry for long-term equity growth, staying anchored in a sound strategy allows us to navigate these periods without losing sight of the larger opportunities. Our team remains focused on keeping your portfolio aligned with these trends as we navigate this evolving landscape together.

Les Vasvari, CFA, CMT

Chief Investment Officer

SAX Wealth Advisors

IMPORTANT DISCLOSURES

This commentary is provided by SAX Wealth Advisors, LLC, an SEC-registered investment adviser, for informational and educational purposes only. It does not constitute investment, tax, or legal advice and should not be relied upon as the basis for any investment decision. The views expressed reflect the analysis and opinion of SAX Wealth Advisors as of the date of publication and are subject to change without notice.

Index and asset class returns referenced are total returns of broad market indices and do not represent the performance of any SAX Wealth Advisors client account, composite, or model portfolio. Indices are unmanaged, do not reflect the deduction of fees or expenses, and cannot be invested in directly.

Past performance is not indicative of future results. Diversification does not guarantee a profit or protect against loss in declining markets. Investing involves risk, including possible loss of principal.

Sources: FactSet Research Systems, Earnings Insight (May 1, 2026); FactSet asset class performance data (April 30, 2026); RBC Global Asset Management, MSCI, and Bloomberg (March 2026).