February Market and Tax Review

In this month’s update, Chief Investment Officer Les Vasvari shares his perspective on the shifting market landscape and what the recent broadening of market leadership may mean for investors. To help you navigate these shifts from a total-wealth perspective, we have also included insightful commentary from our in-house tax expert, Gregg Munn, on tax liability considerations investors may wish to review as tax day approaches.

Market Review with CIO, Les Vasvari

February saw a meaningful continuation of the market regime shift we have been witnessing over the past several months. Equity performance has broadened significantly, moving beyond the borders of the U.S. and into previously overlooked pockets of the domestic market. This transition is a stark departure from the one-sided, mega-cap tech trade that dominated the prior decade.

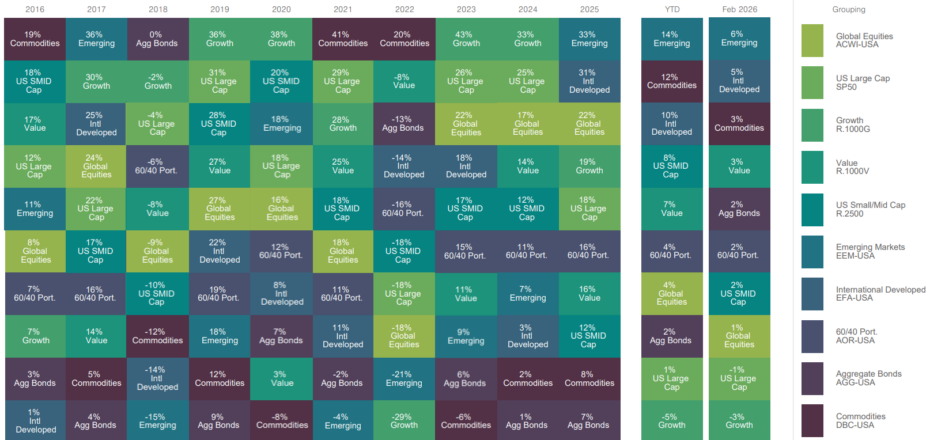

The asset class performance “quilt” included below highlights returns across a range of asset classes over the past 10 years. While leadership shifts meaningfully from year to year, the quilt illustrates how diversified portfolios have historically helped smooth returns over full market cycles.

Source: FactSet, as of February 28, 2026

February Market Highlights

- International Leadership: Non-U.S. equities continued to outpace domestic markets, fueled by aggressive fiscal updates abroad.

- The Tech Recess: Growth and Technology remained the weakest segments as AI optimism wanes, sparking specific valuation concerns within the software industry.

- Broadening Breadth: Market leadership expanded into defensive and cyclical sectors, with smaller-cap companies beginning to outperform their larger counterparts.

- Fixed Income Resilience: Treasury yields declined for much of the month; despite a late-month spike in volatility, U.S. bonds outperformed global equities in February.

Navigating Geopolitical Headwinds

The month opened with a landmark political shift in Japan. Prime Minister Sanae Takaichi’s snap election victory delivered the first two-thirds supermajority since the Second World War, bringing promises of significant fiscal stimulus that have buoyed international sentiment.

In the U.S., the Supreme Court’s decision to strike down portions of the administration’s tariff framework prompted a swift pivot to alternative measures. While the legal maneuvering continues, the net effect appears modest, with effective tariffs currently tracking slightly lower than they were prior to the ruling.

Finally, the month closed with the U.S. and Israel engaging Iran in an armed conflict aimed at regional regime change, a move echoing the events in Venezuela this past January. Unlike the swift transition in Caracas, this engagement may evolve into a longer-duration conflict that could affect regional stability and commodity prices.

The Path Forward

It is vital to remember that markets are historically resilient; they tend to look through these “clouds of uncertainty” to focus on economic fundamentals. Corporate earnings growth remains robust and, crucially, is finally broadening beyond a handful of tech giants. While employment data has softened, it still points toward moderate growth rather than a contraction.

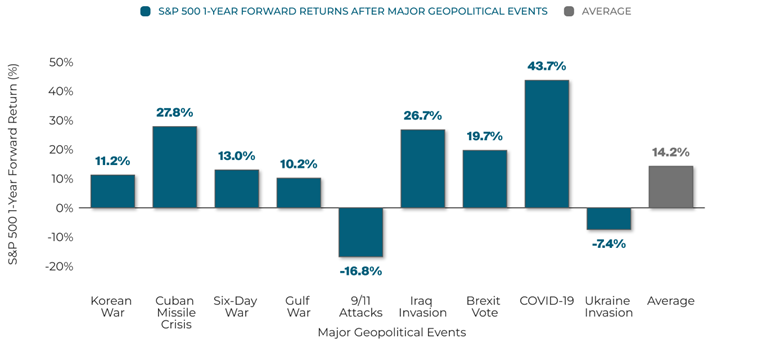

As shown in the chart below, markets have historically performed strongly in many cases, often exceeding historical averages, one year after major geopolitical shocks. While we expect heightened volatility typical of a midterm election year, we view these periods as opportunities for long-term positioning rather than causes for alarm.

Source: © Exhibit A, FactSet Research Systems Inc., Standard & Poor’s.

Definitions & Methodology: The S&P 500 tracks the performance of 500 large-cap U.S. companies, serving as a benchmark for the U.S. stock market. The index is weighted by market capitalization. The chart shows the S&P 500 return 1-year after major geopolitical events historically. Returns are price returns. The chart illustrates that geopolitical conflicts, historically, have not deterred the S&P 500 on average. Dates are: Korean War: 06/25/1950, Cuban Missile Crisis: 10/16/1962, Six-Day War: 6/5/1967, Gulf War: 8/2/1990, 9/11 Attacks: 9/11/2001, Iraq Invasion: 3/20/2003, Brexit Vote: 6/24/2016, COVID-19: 3/11/2020, Ukraine Invasion: 2/24/2022.

Tax Update with Tax Advisor, Gregg Munn, Jr.

With the April 15, 2026 deadline looming, the final month is less about “planning” and more about “precision.” This 2026 tax season is particularly nuanced due to the implementation of the One Big Beautiful Bill Act (OBBBA), which has introduced several new hurdles and opportunities.

The following is a checklist of high-impact reminders that investors may wish to review with their tax professionals:

1. The OBBBA “New Realities” Check

The 2026 filing season (for the 2025 tax year) is the first to reflect several OBBBA adjustments. Investors should verify these three areas with their CPAs immediately:

- The Senior Tax Credit: If you (or your spouse) are 65 or older, you may be eligible for a new $6,000 deduction ($12,000 for joint filers). Note that this phases out starting at $75,000 AGI ($150,000 for joint), so many of you may be disqualified, but it’s worth a final verification.

- SALT Cap Adjustments: The State and Local Tax (SALT) cap has been indexed for inflation. Ensure your preparer is using the updated 2025 limits rather than the legacy $10,000 figure. If your income is between $500k – $600k, the new deduction will be reduced. If your income is over $600k, you will be using the prior $10,000 legacy figure.

2. Last-Call Contributions (The April 15 Deadline)

While most tax strategies ended on December 31, a few “time machines” still exist to lower the 2025 taxable income:

- IRA & HSA Funding: You have until April 15 to max out Traditional IRAs and Health Savings Accounts (HSAs) for the 2025 tax year. For 2025, the HSA limit was $4,300 for individuals and $8,550 for families (plus a $1,000 catch-up for those 55+).

- SEP-IRA & Solo 401(k): If you are self-employed or have a side entity, you can generally fund these plans up until the filing deadline (including extensions), subject to plan rules and eligibility.

3. The “K-1” Waiting Game

For investors in private equity, hedge funds, or LPs, the most common April stressor is the delayed Schedule K-1.

- Proactive Extension: If you haven’t received all K-1s by now, you may want to discuss filing an extension (Form 4868) with your tax preparer.

- Estimated Payment: Remember, an extension to file is not an extension to pay. You must estimate your 2025 liability and pay it by April 15 to avoid interest and failure-to-pay penalties.

4. Net Investment Income Tax (NIIT) Verification

With markets having shifted significantly over the last year, many investors may find themselves subject to the 3.8% NIIT on investment income.

- The Thresholds: Ensure your team has accurately calculated this if your MAGI exceeds $200,000 (single) or $250,000 (married filing jointly).

5. Gift Tax Reporting (Form 709)

Some people tend to overlook the reporting requirements for the Annual Gift Tax Exclusion.

- If you gave more than $19,000 to any one individual in 2025 (or $38,000 for a married couple “splitting” gifts), you must file Form 709. While no tax may be due (as it counts against your lifetime exemption), the filing is a mandatory compliance step to protect your estate plan.

Closing Thoughts

February’s review highlights two important themes for investors right now. From a market perspective, Les notes that leadership is broadening beyond the mega-cap technology names that dominated the past decade, reinforcing the value of diversification and long-term positioning through periods of volatility. On the tax side, Gregg reminds us that as the April 15 deadline approaches, attention to detail matters – particularly with new provisions under the OBBBA and last-minute opportunities such as IRA and HSA contributions.

If you would like to discuss how these market shifts or tax considerations may impact your personal financial plan, please don’t hesitate to reach out to your SAX Wealth Advisors team. We are always here to help you navigate both the opportunities and complexities ahead.

Disclosure: SAX Wealth Advisors, LLC is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. The information contained in this newsletter is for informational and educational purposes only and should not be construed as investment, tax, or legal advice. Clients should consult their tax professional regarding their individual circumstances.