Once is Enough: The New Math Behind Charitable Bunching

Bunching – the tax strategy of grouping more than one year’s worth of charitable donations into a single tax year – gained widespread popularity after the Tax Cuts and Jobs Act of 2017 (TCJA). The TCJA nearly doubled the standard deduction from $6,350 to $12,000 for individual filers and from $12,700 to $24,000 for married filing jointly. This effectively eliminated the itemized deduction benefit for many taxpayers who could no longer clear the standard deduction hurdle. Bunching emerged as a strategy to effectively utilize charitable giving by consolidating multiple years of giving into a single tax year. This enabled the taxpayer to clear the standard deduction hurdle, thereby preserving the tax benefit of their generosity. It remains a widely used strategy today, often in conjunction with a donor advised fund.

With the enactment of the One Big Beautiful Bill Act (OBBA) in 2025, bunching is relevant again – but this time for a different reason and a different group of taxpayers.

A New Floor on Charitable Deductions

Beginning in 2026, OBBBA imposes a floor on the charitable deduction for those taxpayers who itemize. Under the new rules, taxpayers may only earn a charitable deduction for contributions in excess of 0.5% of adjusted gross income (AGI). For C corporations, this floor is 1%. In essence, therefore, the first 0.5% of the taxpayer’s charitable contribution is “wasted” from a deduction standpoint.

This has meaningful impact for high-income donors who already clear the standard deduction hurdle. The post-TCJA bunching rationale targeted taxpayers who couldn’t itemize. In contrast, the new post-OBBBA bunching opportunity targets taxpayers who already itemize and give charitably each year.

Why Bunching Still Makes Sense

By concentrating multiple years of charitable giving into a single tax year, the donor incurs the 0.5% “waste” only once for the bunching period, rather than each year. The tax savings from this strategy can then be redirected toward additional charitable giving, compounding the impact over time.

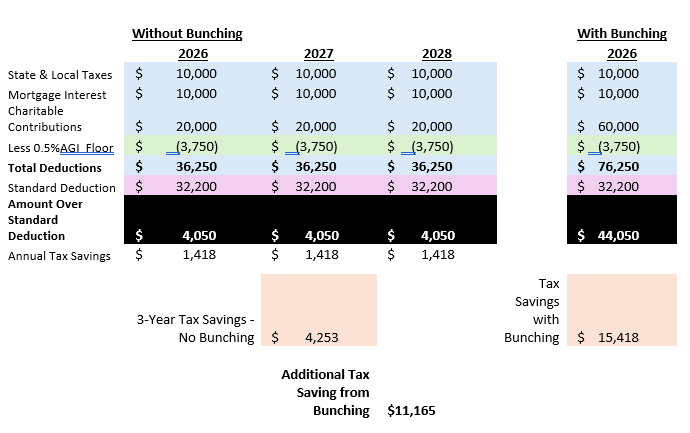

The hypothetical table below illustrates the difference. It assumes a married couple filing jointly with $750,000 in AGI in the 35% income tax bracket. At this income level, the enhanced SALT deduction under OBBBA is fully phased out, limiting SALT deduction to $10,000.

In this hypothetical scenario, bunching results in an estimated additional tax savings of $11,165 over a three-year period.

A Note on High-Income Taxpayers in the 37% Bracket

Taxpayers in the 37% income tax bracket are subject to an additional limitation under OBBBA, which reduces the benefit of itemized deductions from $0.37 to $0.35 per dollar. Bunching can still make sense for this group – the structural advantage of incurring the 0.5% “waste” only once remains intact – but the magnitude of savings may be somewhat diminished from what is illustrated above.

If you have questions about bunching or think it might make sense for you, please reach out to your financial advisor.

About the Author

Tamara M. Paulun, JD, CTFA

Tamara is Director of Advanced Planning & Trusts at SAX Wealth Advisors, LLC where she leads the firm’s estate, trust, and fiduciary planning strategies for high-net-worth individuals, athletes, artists, and multi-generational families. As an attorney and Certified Trust and Financial Advisor, she combines a legal background with deep fiduciary expertise to advise on complex wealth transfer and legacy planning strategies.

Tamara can be reached at tpaulun@saxwa.com or (574) 348-8813.

Disclosure

This material is for informational and educational purposes only and should not be construed as personalized investment, tax, or legal advice. The strategies discussed may not be suitable for all individuals. You should consult your tax advisor regarding your specific situation before implementing any strategy discussed herein. This material contains hypothetical illustrations that are based on assumptions and are not indicative of actual client results. No representation is being made that any client will or is likely to achieve similar results. Actual outcomes will vary based on individual circumstances, including income, tax status, and changes in applicable law. Tax laws and regulations are subject to change, and their application may vary. The information presented is based on current interpretations of the law as of the date of publication and may change in the future.