Q1 2026 Market Review

The first quarter of 2026 was a tale of two trends. The year began with a continuation of the “regime shift” from late 2025, marked by strength in International and Emerging Markets. However, momentum stalled in March as geopolitical tensions and an energy spike altered the landscape, testing resolve with headlines ranging from tech disruption fears to private credit stress.

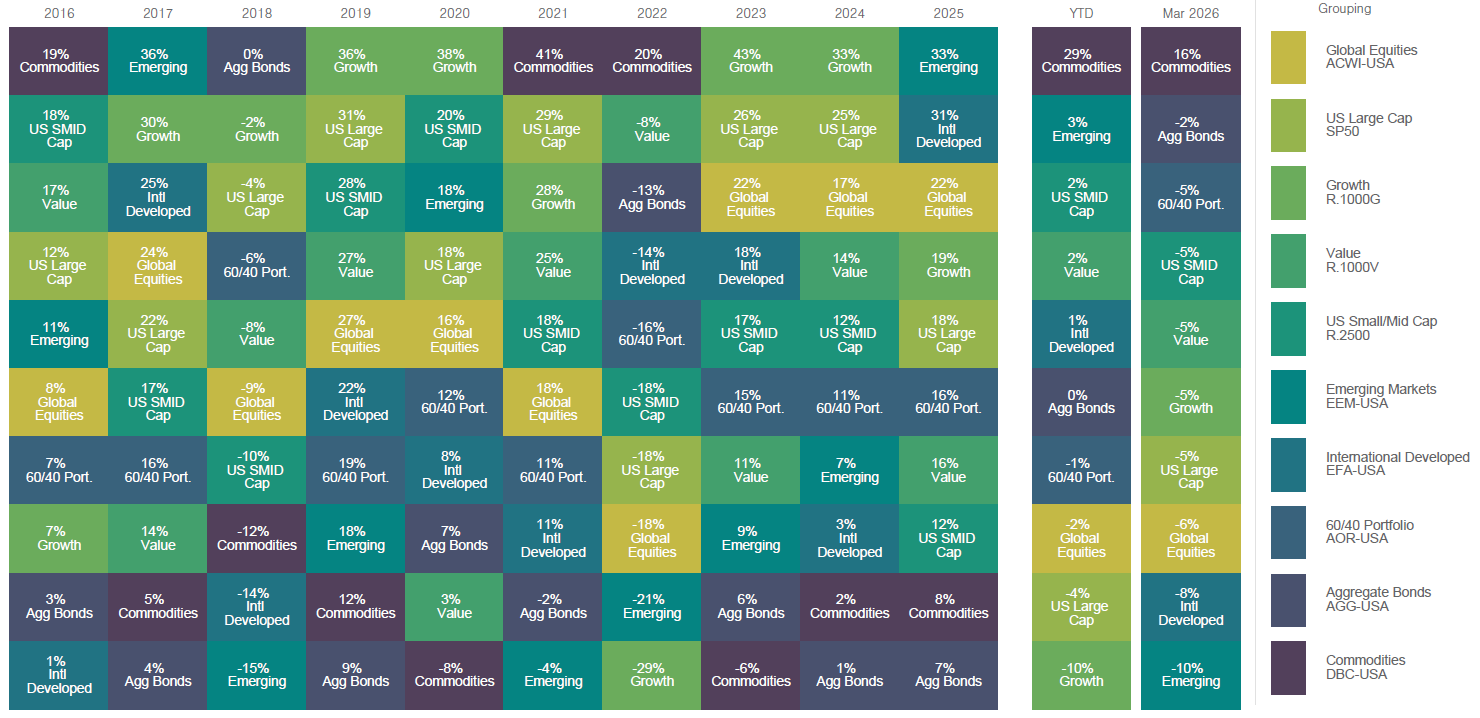

The asset class performance “quilt” included below highlights returns across a range of asset classes over the past 10 years. While leadership shifts meaningfully from year to year, the quilt illustrates how diversified portfolios have historically helped smooth returns over full market cycles.

Source: FactSet, as of March 31, 2026

Q1 Market Highlights:

- Commodities Strength: Driven by the surge in energy prices, commodities were the clear YTD leader, posting a +29% return. In March alone, this asset class gained +16%.

- The Growth Lag: Conversely, the high-flying Growth and US Large Cap sectors of 2025 became the laggards of Q1, finishing the quarter at -10% and -4% respectively, as AI optimism met valuation reality.

The March Pivot: An Orderly but Correlated Pullback

While January and February rewarded global diversification, March saw an “unwind” of those trends. As U.S.-Iran tensions escalated, we witnessed a flight to safety that left the U.S. dollar and commodities among the few major areas posting positive returns.

Significantly, March featured a rare and difficult environment where stocks and bonds went down together. The Aggregate Bond index fell -2% while global equities saw a correlated sell-off. In this downturn, US SMID Cap and Value emerged as relative leaders. While they were down -5% for the month, they held up much better than International Developed (-8%) and Emerging Markets (-10%), which saw their early-year gains evaporate.

However, all things considered, this pullback remained remarkably orderly. We did not see the hallmarks of a systemic panic; rather, we saw a rational repricing of risk. The resulting surge in energy prices, with Brent crude posting its largest monthly gain since the 1970s, reignited inflation concerns, yet several underlying economic indicators have remained relatively resilient:

- Real Terms vs. Nominal: While nominal prices surged toward $120 a barrel, when adjusted for inflation, crude oil is still not at an extreme price relative to past crises in 2008 and the late 1970s.

- Decreased Energy Sensitivity: The U.S. economy is far less energy-sensitive today than in past cycles. Consumers spend a smaller share of their income on energy, and recent tax cuts provide a partial buffer.

- The Wage Cushion: Wage growth continues to outpace inflation, meaning real purchasing power is actually expanding despite rising commodity costs.

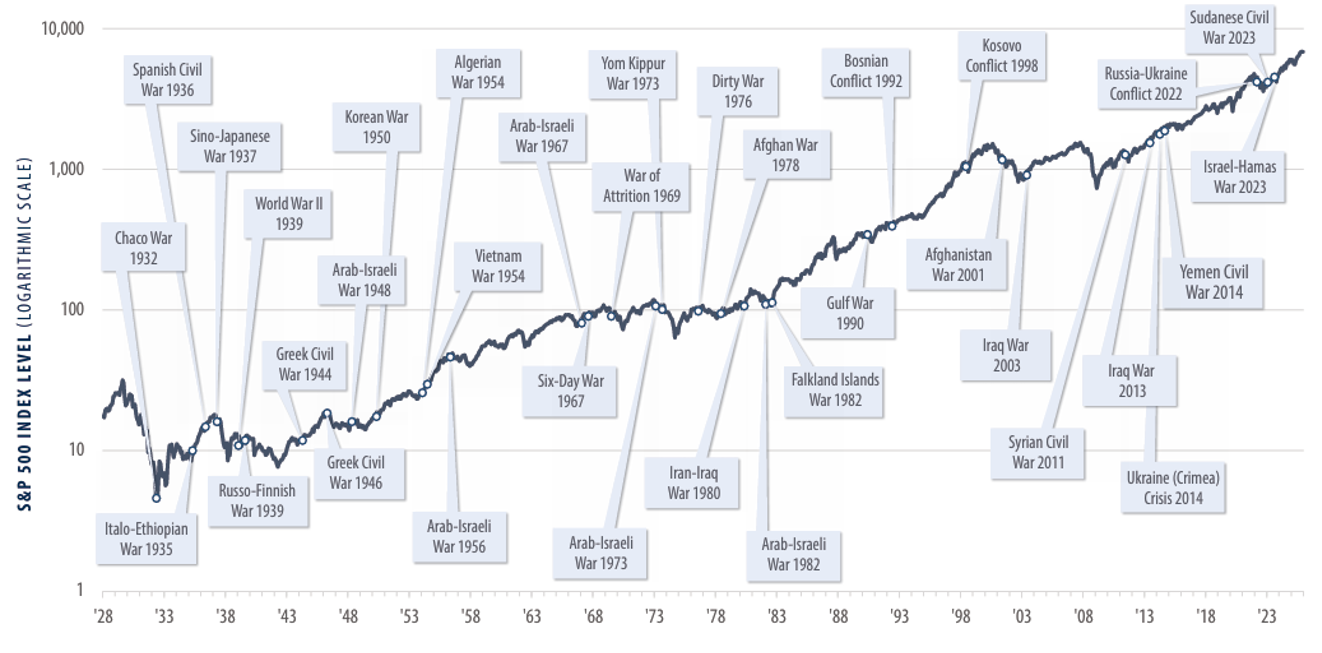

The Behavioral Edge: Volatility as the “Cost of Entry”

In moments like these, it is helpful to remember a fundamental truth of investing: volatility is not a bug; it is the “cost of entry” to experience long-term equity appreciation.

The chart below illustrates this resilience vividly. While uncertainty can influence markets in the short term, the index has historically “looked past” geopolitical conflicts to focus on corporate fundamentals, which remain strong.

The S&P 500 Compounds Over the Long Run Despite Wars

Source: First Trust, S&P CapIQ, Bloomberg, Monthly index levels from 1928-2025

Nevertheless, periods of heightened volatility are excellent times to practice self-awareness. While feeling a degree of discomfort during market drawdowns is perfectly normal, your portfolio shouldn’t be structured in a way that causes you to lose sleep.

Planning Note: This is not a time to make impulsive changes. The heat of a market drawdown is rarely the right moment for a tactical shift. However, once the “dust settles,” it may be a very productive time to reassess with your advisor whether your portfolio’s risk level truly aligns with your long-term comfort.

The Path Forward

Geopolitical “clouds of uncertainty” will always exist, but markets are historically resilient. They eventually look through the headlines to focus on the fact that corporate earnings are growing and that growth is now spread across more sectors than it has been in years.

Furthermore, these drawdownsare historically excellent times to get more positive on the equity markets if we don’t enter a recession. Currently, our “weight of the evidence” continues to point toward resilience in the domestic labor market and robust corporate capex, which supports our constructive long-term outlook.

Thank you for your continued trust as we navigate these conditions together.

Warm regards,

Les Vasvari, CFA, CMT

SAX Wealth Advisors, LLC is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. The information contained in this newsletter is for informational and educational purposes only and should not be construed as investment, tax, or legal advice. Clients should consult their tax professional regarding their individual circumstances.