Q2 2026 MARKET REVIEW

I hope everyone enjoyed a wonderful Fourth of July holiday with family and friends. Celebrating Independence Day always serves as a great reminder of American resilience. Back in 1776, the United States was the ultimate underdog, facing off against the world’s most dominant empire with little more than a raw conviction in its own long-term potential.

I can’t help but notice a clear parallel in how financial markets functioned during the second quarter of 2026. For the past year, the “S&P 493,” representing the broader market outside of the dominant mega-cap technology giants, and smaller-cap companies have been treated like the market’s underdogs. Conventional wisdom suggested that a hawkish Federal Reserve transition under new Chair Kevin Warsh and high interest rates would completely stall their progress. Yet, just like those early American underdogs, these overlooked asset classes staged a powerful, quiet revolt.

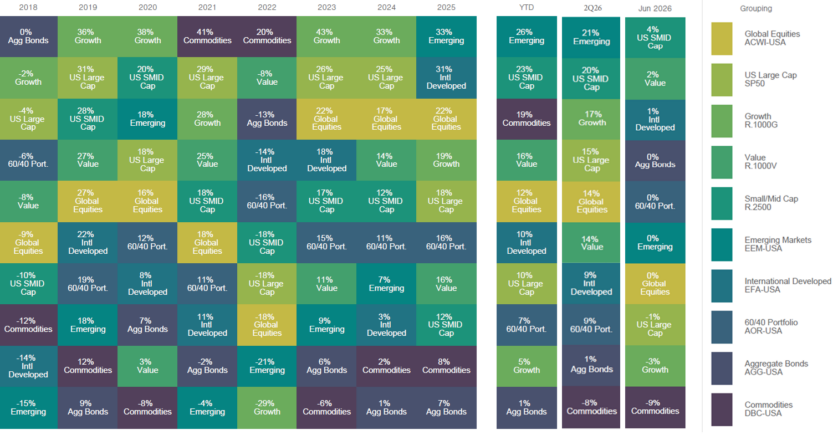

The asset class performance “quilt” included below highlights returns across a range of asset classes over recent years. While leadership shifts meaningfully from year to year, the quilt illustrates how diversified portfolios have historically helped smooth returns over full market cycles.

Source: FactSet, as of June 30, 2026

SECOND QUARTER MARKET HIGHLIGHTS

- Emerging Markets Skyrocket: Emerging markets led global equity regions for the quarter with a massive 21% return in 2Q26, driven by exceptional earnings in the Asian technology supply chain.

- Underdog SMID Cap Surges: US Small/Mid-Cap (SMID) equities gained 20% over the quarter and led all asset classes in June with a 4% monthly return, a massive 7% spread over Large Cap Growth for month. The sub asset class was fueled by risk-on sentiment as Middle East tensions eased and historically low starting valuations.

- Growth Factor Rebounds: Growth assets gained 17% in 2Q26 as global hyperscalers raised their 2026 AI infrastructure capex guidance to an impressive USD 700 billion. Both the S&P 500 (up nearly 15%) and the Nasdaq (up nearly 21.5%) had their best single quarterly performances since the second quarter of 2020.

- Value Equities Advance: Value benchmarks reasserted themselves in June (+2% return) as investors rotated out of extended growth positions and into areas sensitive to economic resilience.

- Commodities Face Stiff Headwinds: Commodities fell 8% in Q2, finishing as the worst quarterly performer. It is a fitting twist of history that our national icon, Uncle Sam, was originally inspired by a 19th-century meatpacker stamping barrels of raw beef. Had he been packing provisions this quarter, tight livestock inventories would have forced him to stamp them with record-high cash prices. For the broader index, however, energy drove the downside pressure; Brent crude plummeted from its April peak of USD 120 per barrel back toward the USD 70 range, fully reversing the war rally as traders rapidly unwound defensive hedges.

THE DICHOTOMY OF THE UNDERDOGS

The defining feature of 2Q26 was a dramatic role reversal within equity markets. For several quarters, mega-cap technology and the Magnificent Seven dominated performance. The script flipped as pockets of extended mega-cap growth underwent profit-taking and market leadership expanded into small-caps, micro-caps, and value benchmarks, propelling the broader market to new all-time highs even as the market’s previous leaders took a backseat. It turns out that the broader domestic economic engine had plenty of fuel left in the tank, suggesting that corporate strength extends far beyond just a handful of technology giants.

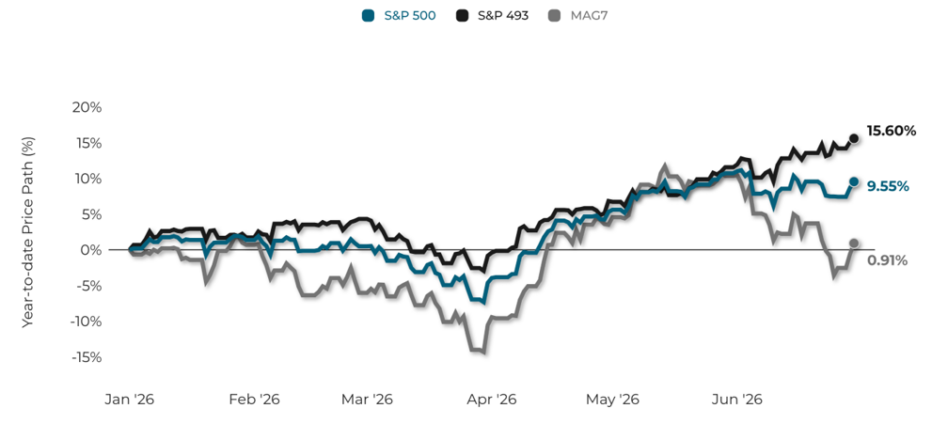

The historical price chart below visually illustrates this stark market dichotomy that defined the first half of 2026. Note the bifurcation in June, in particular, as the S&P 493 appreciated while the Mag7 sank:

Source: © Exhibit A, FactSet Research Systems Inc., Standard & Poor’s

Definitions & Methodology: The S&P 500 tracks the performance of 500 large-cap U.S. companies, serving as a benchmark for the U.S. stock market. The index is weighted by market capitalization. The chart displays year-to-date price returns of the S&P 500, S&P 493, and Mag7. The Mag7 refers to Apple, Microsoft, Amazon, NVIDIA, Meta Platforms, Alphabet, and Tesla; seven large-cap stocks often cited for their market leadership. The S&P 493 represents the remaining constituents of the S&P 500 after excluding the Mag7. This breakdown highlights the performance gap between the index’s largest names and the broader market. References to specific securities are for illustrative purposes only and do not constitute a recommendation to buy or sell any security.

While SMID cap won the battle against the Mega Cap giants in the 2nd quarter, we’re not yet convinced they have the resilience of the revolutionaries to win the war. Further positive data and relative outperformance would be factors we continue to monitor.

THE POWER OF THE AI SUPPLY CHAIN

Make no mistake: while leadership broadened, the fundamental engine powering the global economy remains the artificial intelligence buildout. The difference in Q2 was that investors became far more selective. Instead of buying generic mega-caps, capital flooded into the companies producing the literal “picks and shovels” of the AI boom, specifically the semiconductor and electrical equipment manufacturers.

- The Semiconductor Record: The Philadelphia Semiconductor Index (SOX) rocketed an astonishing 87.8% higher in Q2, marking its best quarterly performance since inception in 1994.

- The Asia Ex-Japan Boom: Asia ex-Japan returned a spectacular 28% for the quarter, led by Korea (+88%) and Taiwan (+49%). Heavyweights SK Hynix and Samsung Electronics doubled and tripled in value, joining the exclusive USD 1 trillion market cap club and driving Korean equities to their best quarterly showing since 1998.

References to specific securities (including SK Hynix and Samsung Electronics) are for illustrative purposes only and do not constitute a recommendation to buy or sell any security.

NAVIGATING INSTITUTIONAL AND GEOPOLITICAL WINDS

While corporate fundamentals remain exceptionally strong, we are mindful of a shifting institutional landscape. In his initial meetings as Fed Chairman, Kevin Warsh struck a surprisingly hawkish tone at the June FOMC meeting. Driven by May core PCE inflation rising for a third consecutive month to 3.4%, the Fed expressed greater near-term inflation concerns than expected, driving markets to anticipate about 1 rate hike by year-end.

History notes that financial markets almost always “test” a new Fed Chair with near-term policy uncertainty and localized volatility. Warsh is accelerating this pattern by actively pushing to scale back “forward guidance” and alter communication strategy, deliberately forcing Wall Street to break its addiction to explicit central bank hand-holding.

Normally, a hawkish transition would rattle markets, but accelerating corporate profitability has acted as an effective buffer. According to FactSet, Q2 year-on-year revenue growth expectations have climbed to 12.3%, while earnings growth expectations have risen to 23.1%. This combination of accelerating top-line revenue and expanding profit margins gives the bull market a firm fundamental anchor, in our view, despite the shifting winds in Washington.

CLOSING THOUGHTS

The first half of 2026 has thoroughly challenged conventional wisdom. It showed that the market can climb to record heights without relying exclusively on a handful of tech giants, and it demonstrated that the broader market’s “underdogs” were still in the fight.

While we expect typical election-year volatility and seasonal bumps as the summer progresses, in our view, the weight of the evidence tells us that this expansion is fundamentally supported by real earnings power. True financial independence requires the discipline to stick with a well-diversified global allocation even when certain sectors look like underdogs on the surface. Enjoy the rest of your July, keep the grill hot, and know that our team is always here to help you manage the complexities of this evolving market terrain.

Les Vasvari, CFA, CMT

Chief Investment Officer

SAX Wealth Advisors

SAX Wealth Advisors, LLC is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. The information contained in this newsletter is for informational and educational purposes only and should not be construed as investment, tax, or legal advice. Clients should consult their tax professional regarding their individual circumstances.