MAY 2026 MARKET REVIEW

The weather is heating up outside, and financial markets are matching the temperature following a remarkable nine-week winning streak that has propelled the S&P 500 to new all-time highs. This fundamental earnings momentum leads us into a summer of highly anticipated, high-heat milestones, including the SpaceX IPO on June 12, which naturally raises the question of whether the market will safely sizzle or risk overheating. Speaking of rising temperatures and high-heat milestones, my family’s upcoming move (that I referenced in my introductory letter) from Queens to the New Jersey suburbs is officially happening in a couple of weeks. While it will be bittersweet to leave behind the vibrant energy of the city I grew up in and we’ve loved calling home, I’m fired up for the grilling season ahead.

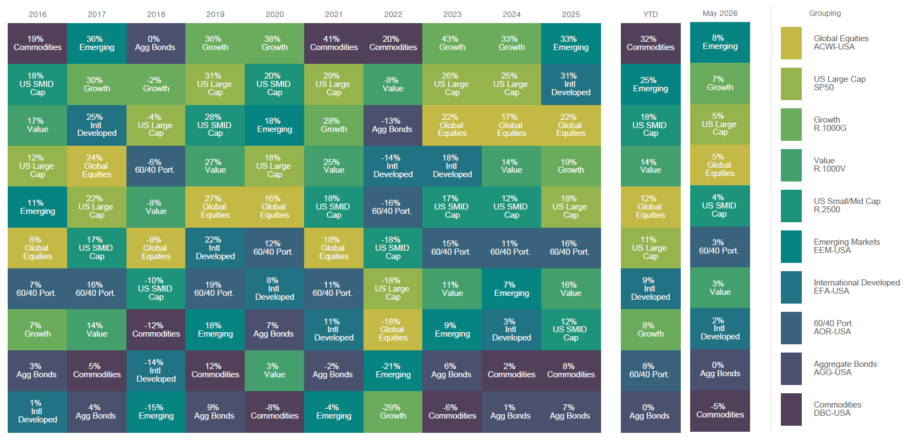

The asset class performance “quilt” included below highlights returns across a range of asset classes over the past 10 years. While leadership shifts meaningfully from year to year, the quilt illustrates how diversified portfolios have historically helped smooth returns over full market cycles.

The asset class returns shown represent the performance of broad, unmanaged market indices and do not reflect the performance of any SAX Wealth Advisors client account, composite, or model portfolio.

May Market Highlights

- Emerging markets led all asset classes with an 8% return, driven by exceptional earnings in the Asian technology supply chain. As discussed in April, we remain constructive on this region as it attempts a structural breakout from a multi-year secular low.

- Growth assets followed close behind with a 7% gain, re-energized by a resurgence in software names alongside the broader artificial intelligence tailwind.

- Commodities were the weakest segment, losing 5%. Brent crude oil plummeted -19% as easing Middle East tensions and progress toward an Iran ceasefire led traders to unwind defensive hedges, leaving the global supply outlook more balanced.

The Fundamental Engine: AI and Corporate Earnings

May’s rally was driven by real profit growth rather than speculative expansion, capped by a 28.6% blended earnings growth rate, the fastest since late 2021. Artificial intelligence remains the key engine, driving nearly 70% of global equity gains as tech investment approaches 5% of GDP. Data center and semiconductor spending supported margins, but investors are becoming more selective. Nvidia still sees strong demand, while sentiment toward other tech giants has cooled amid scrutiny over AI infrastructure returns. Overseas, Asia earnings surged 40%, led by Taiwan and South Korea.

Strength Begets Strength: Analyzing the Data

To understand the historical implications of the momentum we’ve experienced, I analyzed periods since 1970 when the S&P 500 surged 15% or more over six weeks (triggered on May 11). Historically, such strong upward price momentum has pointed to long-term health rather than exhaustion. Following these surge events, the index generated a 19.0% average forward 12-month return and a 21.7% median return. Downside risk was also well-contained, with an average maximum drawdown of -11.9% and a median drawdown of -9.3% over the following year. This contrasts with the S&P 500’s baseline of about 9% returns with a deeper average drawdown of -14%.

Source: Yahoo Finance. Calculations performed using internal SAX Wealth Advisors analysis. Data believed to be reliable but not guaranteed.

Navigating Seasonal and Institutional Risks

We must balance this enthusiasm against near-term risks. As I’ve mentioned before, midterm election years like 2026 are historically volatile, carrying an average intra-year drawdown of -17.5%. Furthermore, markets tend to test new leadership; Kevin Warsh took office as Fed Chair on May 22nd, and the year following a new chair historically sees an average drawdown that matches that same -17.5% figure. After this massive run-up, the market’s ability to absorb negative surprises is naturally reduced. Currently, the S&P 500 is up 11% year-to-date and has experienced just 1 pullback with a -9% drawdown. Monitoring interest rates and global energy infrastructure remains a core focus.

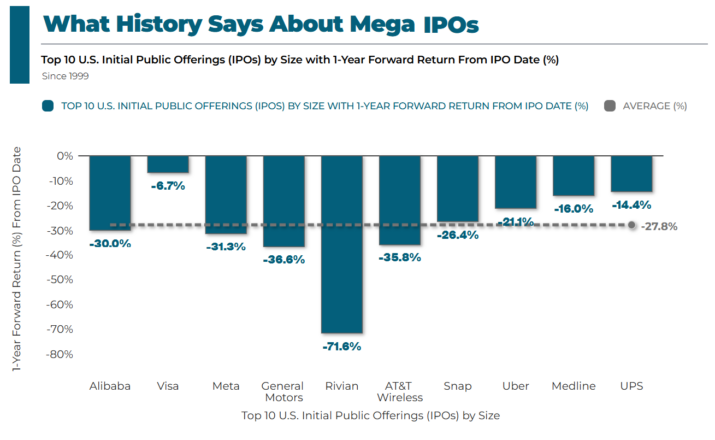

The Mega-IPO Wave: SpaceX and the Insider Game

The upcoming SpaceX mega-IPO on June 12 is dominating headlines, with speculations around OpenAI and Anthropic eventually following suit. While public issuance waves inject enthusiasm, they also add equity supply and localized volatility.

History offers an essential lesson: first-day trading gains, when they occur, often accrue to investors who receive share allocations before public trading begins; investors purchasing after trading opens may experience materially different risk and return outcomes, and long-run buy-and-hold strategies for mega-IPOs have historically underperformed. As highlighted in the performance chart below, one year after their debuts, the top ten largest U.S. IPOs historically averaged a -27.8% return, with significant underperformance across major names like Alibaba (-30.0%) and Facebook (-31.3%).

Source: © Exhibit A, FactSet Research Systems Inc. The IPO returns shown are historical and are not indicative of future results. References to specific companies or offerings are for informational purposes only and are not a recommendation to buy, sell, hold, or avoid any security, including any initial public offering.

The Path Forward

While we anticipate periodic seasonal pullbacks and transition volatility, it’s our opinion that this bull market deserves the benefit of the doubt. Success requires looking past short-term noise and maintaining a well-diversified global allocation. As the summer heat settles in and our family packs for New Jersey, now is the perfect time to step away from the daily ticker, reach for a frosty beer or an icy lemonade, and enjoy some time to cool down.

Les Vasvari, CFA, CMT

Chief Investment Officer

SAX Wealth Advisors

Disclosures

This commentary is provided by SAX Wealth Advisors, LLC, an SEC-registered investment adviser, for informational and educational purposes only. It does not constitute investment, tax, or legal advice and should not be relied upon as the basis for any investment decision. The views expressed reflect the opinion of SAX Wealth Advisors as of the date of publication and are subject to change without notice.

Index and asset class returns referenced are total returns of broad, unmanaged market indices and do not represent the performance of any SAX Wealth Advisors client account, composite, or model portfolio. Indices cannot be invested in directly and do not reflect the deduction of advisory fees, transaction costs, or taxes.

Past performance is not indicative of future results. Diversification does not guarantee a profit or protect against loss in declining markets. Investing involves risk, including the possible loss of principal.

Any references to specific companies, securities, sectors, or initial public offerings are for informational purposes only and should not be construed as a recommendation to buy, sell, hold, or avoid any security.

Certain information has been obtained from third-party sources believed to be reliable; however, SAX Wealth Advisors does not guarantee its accuracy or completeness.