Sep 09, 2020 - Income Planning and IRMAA in Retirement

Medicare is an area that practically every American will encounter when planning for retirement. It sits at the intersection of health and wealth in your financial life plan, and so often surfaces across a range of long-term planning conversations. Plus, Medicare and its associated costs can be a confusing topic, given the program’s various parts, costs and benefits. With approximately 10,000 Americans becoming eligible for Medicare every day, navigating these decisions in a cost-effective manner can be a daunting task without some guidance.

Medicare Coverage Options: The Basics

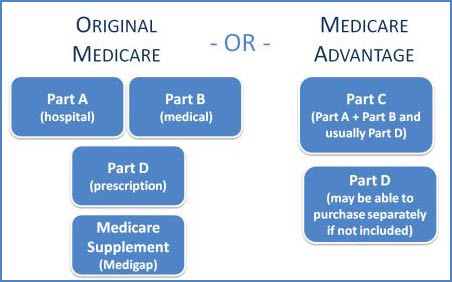

Simply put, Medicare generally has two main enrollment options, which include five main components. Everyone signs up for Parts A and B, and then, to help cover what Parts A and B do not, you have a choice between a Medicare Supplement Plan (also called a Medigap Plan) and Part D on one hand or a Medicare Advantage Plan on the other. The following diagram illustrates how these two enrollment options fit together.

Medigap Plans (the first route you could take) are typically more expensive than a Medicare Advantage Plan (typically your second option), but provide more overall coverage. While Medigap Plans are offered by private insurance companies, plan benefits are regulated by Medicare regardless of what company you buy coverage from. The only variable is the premium that each company charges. Your Medigap Plan will be accepted anywhere that original Medicare is accepted, which can offer welcome peace of mind. What’s more, you aren’t restricted to specific doctors and generally do not need a referral to see a specialist. While the plan premiums may cost more, you know you will almost certainly have coverage should any medical issue arise in the future and additional out-of-pocket costs will be limited.

Medicare Advantage Plans (that is, Part C) have been gaining attention because they are marketed as a no- or low-cost option that wraps everything into one plan. Think of these plans as a Medicare HMO. While many of these plans do provide additional benefits, such as dental or vision, you should keep a few things in mind. Medicare Advantage Plans usually work within a network of preferred doctors and hospitals, require referrals to see a specialist, and they are not always accepted by all health-care providers. Also, if you travel, even within the U.S., there is a big chance your plan will not be accepted in other states, possibly resulting in higher out-of-pocket costs if you need medical care away from home. Lastly, these plans can change yearly, so you’ll need to review them annually to ensure the plan you have is still a good fit for your needs.

The Cost Part of Your Equation

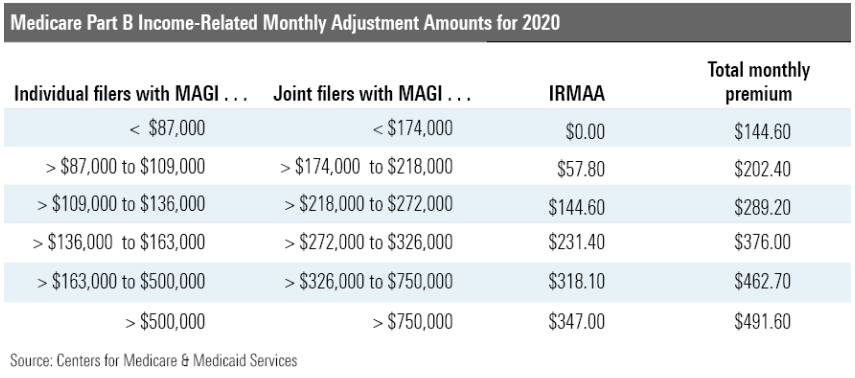

Besides considering what coverage to apply for, it’s important to be aware of the potential costs associated with Medicare. While most people pay the standard monthly Part B premium of $144.60 and their Part D premium for medical and prescription drug coverage, if your income is above a certain limit, extra surcharges will likely apply.

Due to the Bipartisan Budget Act of 2018, if you are considered a high earner or you are an individual with modified adjusted gross income (MAGI) greater than $87,000 or a married couple filing jointly with MAGI greater than $174,000, you will have additional charges that apply to your Part B and Part D premiums. Medicare refers to these surcharges as income-related monthly adjustment amounts (IRMAAs). The premiums for 2020 vary from an additional $57.80 to $347 for Part B and $12.20 to $76.40 for Part D.

Medicare uses your income from your tax return from two years ago to determine your premiums for the current year. This means your 2021 premiums will be based on your 2019 MAGI. This information is shared annually between the Social Security Administration and the IRS, so there is no way to avoid these reviews.

The next time you find yourself in an income tax planning conversation, keep this two-year look-back in mind. If you have future income coming in a lump sum, such as from selling a business or cashing out on restricted stock, you may want to consider taking those payouts more than two years prior to signing up for Medicare, if possible, to avoid paying these surcharges. The good news for people who are in this situation and have received one-time, lump-sum income is that they will only pay a higher amount for one year, as new premiums are calculated annually.

Once you’ve signed up for Medicare, you should receive a notice letter from the Social Security Administration toward the end of each year with your premium amounts for the next year. There are specific instances in which you can file an appeal to have your IRMAA adjusted, but generally these are limited to certain major life events, such as you recently stopped working, marriage, divorce, or death of a spouse.

When planning for what your retirement might look like, keep these IRMAA adjustments in mind and consider strategies that may help you avoid paying these additional surcharges. Going just $1 into the next tier means paying that larger surcharge for an entire year. Viewing IRMAA in the context of your financial picture as a whole and in conjunction with various income planning and tax strategies – from making qualified charitable distributions and funding a health savings account to the timing around when to realize capital gains/losses and take Social Security benefits – could play a part in potentially reducing your health-care expenses in retirement.